Navigating Stock Option Repricing in the Face of Falling 409a Valuations

409a valuations for many privately held tech companies have fallen since the end of 2021. As a result, canceling existing stock option grants and reissuing them at the new, lower 409a has become a common occurrence. In this blog post, I'll dive into what this means for employees and how to navigate the impact of stock option repricing.

Why 409a Valuation Matters to You

When it comes to stock options, the magic number is the 409a valuation. In order to avoid undesirable tax and legal implications, stock options can't be priced lower than the FMV, and the 409a valuation dictates the deemed fair market value (FMV) of a company's stock for the purpose of setting the exercise price of your stock options. This valuation has a ripple effect on your potential gains, your tax liability, and the overall value of your options.

The Reality of Lower Valuations

Privately-held companies, particularly venture-backed tech startups, are generally expected to only see their 409a valuations increase over time. A big reason for this is because unlike public companies which have continuous adjustments to their market prices, private companies don't have open markets for their stock, and 409a valuations are only required to be appraised by an independent third party every 12 months (or when there's a material event). With such infrequent measurement periods and the tendency for the markets, stock prices, and the economy as a whole to trend upward over time, downward revaluations of a company's 409a valuations can come with particularly negative sentiment.

Due to changes in economic conditions and investor sentiment in 2022, public tech stock prices fell broadly and the fundamentals of many private tech companies weakened. This prompted a downward shift in the 409a valuations for many companies. Although a drop in 409a might be concerning in normal circumstances, where your company is the only one veering off the road, you might be able to take some solace in the fact that everyone else is facing similar headwinds. That being said, your company must still be able to withstand the stumbling blocks standing in the way of success. Less enthusiastic investors and customers with tightening budgets mean less money flowing, which can be disastrous even for a company with great traction and amazing offerings.

Facing Stock Option Repricing: What You Should Know

- Understand the impact: Your exercise price may be lowered to match the new 409a valuation, making it less expensive for you to buy company shares.

- Be aware of the risks: A repricing might feel like being able to get shares at a discount, but in reality, it's reflective of the current outlook and perceived future potential of your company.

- Company communication: If your company decides to reprice your options, clear communication is key. They should explain why this decision was made, addressing concerns about your existing options and their revised value.

- Your choice: Your participation in an option repricing might be optional, but in some cases, it might not be. Some employees may prefer not to reprice their options due to personal circumstances or if doing so might have an adverse impact on their future taxes.

- Tax implications: Be aware of potential tax implications resulting from repricing. This shouldn't be an issue with NSOs, but it could be a factor if you have ISOs.

Implications for NSOs

Thankfully, there's not much else to know here. Since the original exercise price on your NSOs is above the current 409a valuation, repricing your exercise price down to the 409a comes with no negative effects. The only disclaimer is that this assumes your company follows all applicable laws when repricing.

Implications for ISOs

Unlike NSOs, ISOs are trickier because they must adhere to a specific set of rules to qualify as ISOs. Repricing options is considered a "modification", which means the repriced grant is treated as a new grant (think of it as canceling your original grant and being issued a new one with a different exercise price). Because repriced ISOs are treated as a new grant, if the repriced grant fails to adhere to those rules, they're disqualified, become NSOs, and lose their qualified tax status.

- New grant date: Your grant date is pulled forward to the date of the repricing. This is important because in order to make a qualifying disposition and retain the tax-advantaged nature of ISOs, a sale must occur more than two years after your ISOs were granted and more than one year after exercise. For example, if your ISOs were repriced on January 1, 2023, the absolute earliest date you can make a qualifying disposition would be on January 2, 2025.

- $100k limitation: No more than $100k of ISOs can first become exercisable in a given year, with any excess being converted to NSOs. The "value" of the ISOs is measured on the grant date and will generally be the exercise price * the number of ISOs that will become exercisable that year. Both your original grant and the repriced grant (along with any other outstanding grants) are considered for the purposes of the $100k limitation. If your grants are large enough, a repricing could force most or all of your repriced grant to become NSOs.

- Original vesting schedule: Most companies opt to retain original vesting schedules to the extent they can so the only change to your ISO grant is the repricing and (forced) new grant date. You should double-check to make sure your original vesting schedule is retained, but also recognize that retaining the original vesting schedule could negatively impact you because of the $100k limitation.

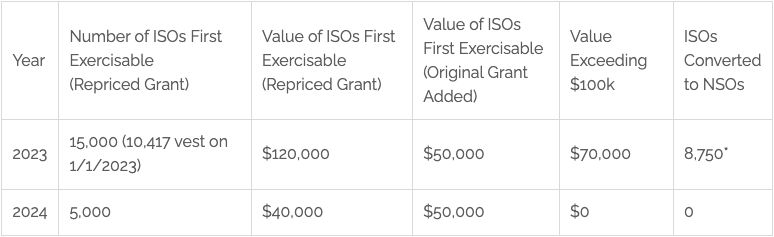

$100k Limitation Example

On January 1, 2021, you were issued 20,000 ISOs with an exercise price of $10 per share. They vest monthly over four years and have a one-year cliff, so 25% plus 1/48th vest on January 1, 2022, and 1/48 vest every month after that. You aren't allowed to early-exercise your options, and this is your only ISO grant.

For the purposes of the $100k limitation, $0 first becomes exercisable in 2021, $100,000 in 2022, $50,000 in 2023, and $50,000 in 2024. There are no excess ISOs that convert to NSOs.

Your company's 409a falls to $8 and your ISOs are subsequently repriced to $8 per share on January 1, 2023. Your original vesting schedule remains, and you haven't yet exercised any of your options. Therefore, your vesting schedule is 50% plus 1/48th vested on January 1, 2023, with 1/48 vesting monthly for the next two years.

For the purposes of the $100k limitation, $120,000 first becomes exercisable in 2023, and $40,000 in 2024. Additionally, since the original grant is also considered, $50,000 is added to both 2023 and 2024, pushing the total amounts to $170,000 for 2023 and $90,000 for 2024.

As a result, you'll have $70,000 of excess ISOs in 2023 that convert to NSOs.

*The number of ISOs converted is based on the new grant price of $8. The last options vesting that year convert first, so work backward from December 31st to determine which options will become NSOs. The result: only the 6,250 options that vest on 1/1/2023 remain ISOs.

Furthermore, if your company gets acquired or goes public and you sell your ISO shares on any date before January 2, 2025, the sale will be a disqualifying disposition because of the "two years from grant" requirement, which could negatively impact your taxes.

Acquisition Example

Continuing the example above, let's say you decided to exercise your 6,250 ISOs on December 1, 2023 after the 409a increased to $12. When filing your taxes for 2023, you determine that no AMT is owed, so your only cost is the $50,000 exercise cost (6,250 * $8). Your company is subsequently acquired for $15/share on December 15th, 2024 (assume all unexercised or unvested options are exchanged for the new company's equity in a non-taxable exchange so we can ignore your NSOs entirely).

The good news is that your ISOs have long-term capital gains treatment because they were held for more than one year. The bad news is that you didn't meet the two-year-from-grant requirement since your grant date was pulled from 2021 to 2023 because of the repricing. This creates a disqualifying disposition and has two tax implications: 1) your exercise spread of $4/share ($12 FMV at exercise - $8 exercise price) is taxable as ordinary income in 2024, and 2) your long-term capital gain is limited to $3/share ($15 sale price - $12 FMV at exercise). Therefore, $25,000 is taxed at ordinary income rates and $18,750 is taxed at long-term capital gains rates.

Assuming an ordinary income tax rate of 32% and a long-term capital gains tax rate of 18.8%, this results in $11,525 of taxes ($8,000 OI + $3,525 LTCG). Netting the proceeds out from your costs, you have $93,750 of pre-tax proceeds from the acquisition, less your $50,000 cost to exercise and $11,525 in taxes, or $32,225 net of all costs and taxes. If your company just held the acquisition off until January 2, 2025, the two-years-from-grant requirement would be met, and there would only be long-term capital gains tax on the full $7/share, or $8,225 in total taxes.

Conclusion

Falling 409a valuations have prompted many privately held tech companies to reprice their employees' stock options. Navigating stock option repricing necessitates a clear understanding of its implications, risks, and careful consideration of your personal circumstances and potential tax consequences, especially in the case of ISOs. While these changes present challenges, they also offer opportunities for strategic financial planning in an ever-evolving market. If you need help navigating your equity compensation, feel free to reach out or schedule a time to talk.

Categories

Have questions about this post?

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod temor.